When you live in a part of the country with a nascent entrepreneurial ecosystem it can be challenging to connect with investors, mentors, and even other entrepreneurs. In smaller markets it often feels like there is less collaboration and/or synergy between participants (investors and entrepreneurs) because individuals on both sides believe they are competing for a limited number of resources. On one hand, many investors don’t share deal flow because they feel like there aren’t enough deals to go around. On the other hand, entrepreneurs don’t readily share their investor contacts because they feel like they are competing with other entrepreneurs for the same investors. It’s a vicious cycle that instills a lack of trust between market participants and incites market fragmentation, neither of which are useful nor beneficial.

I’m assuming this dynamic is present in a lot of smaller markets around the U.S. where the venture capital and entrepreneurial ecosystems aren’t as mature in comparison to places like Silicon Valley, NYC, or Boston. Researchers argue that the creation of entrepreneurial ecosystems must be (or usually are) organic, suggesting that vibrant ecosystems are difficult to recreate through policy or hands-on manipulation. In the paper, “Entrepreneurial Spawning: Public Corporations and the Genesis of New Ventures, 1986 to 1999,” the authors suggest that “the breeding grounds for entrepreneurial firms are likely to be other entrepreneurial firms” and that “stimulating entrepreneurship in a region with few existing entrepreneurial firms is difficult.” They also suggest that “policies that have sought to foster entrepreneurial and venture capital activity by providing capital or investment incentives may not be strong enough. Instead, regions may need to attract firms with existing pools of workers who have the training and conditioning to become entrepreneurs.”

In another paper, “Go West Young Firm: Agglomeration and Embeddedness in Startup Migrations to Silicon Valley, “ the author suggests that location and access to resources are critical components for entrepreneurial growth and productivity. Per the paper, “Agglomeration focuses on how distance from goods, people, and ideas, creates transportation costs that impact productivity. She continues, “Today, the most relevant of these distance costs seems to be the ability of firms to access knowledge. A firm can engage with local customers and employees by simply locating to a specific city: however, learning innovative ideas and tacit information usually requires being so geographically close that people have face-to-face interactions with relevant counterparts.”

These two papers are wonderfully written and I have great respect for the authors who wrote them. However, given that the information used to arrive at these conclusions was based on data from 1986 to 1999 and from 1996 to 2005, I believe new research is needed to more accurately portray how technology and demographic changes have impacted popular entrepreneurial hubs leading to the creation of new tools and mechanisms for accessing entrepreneurial and investor resources in smaller markets.

In my opinion, the growing number of entrepreneurial ecosystems outside of popular entrepreneurial hubs will continue to increase due to the following reasons:

- Technology has made it easier to access talent, resources, and capital, regardless of geographic location.

- The behavioral change and adoption rate of connecting remotely is becoming the new norm in business, especially as a result of the pandemic. (Related Article).

- The cost of living and operating a company in a highly populated, coastal cities is becoming increasingly more expensive (Related Article).

I think the above points speak for themselves and don’t require further explanation. What I think is more helpful is examining the year-over-year change (YoY) in deal count and deal value in specific regions of the country.

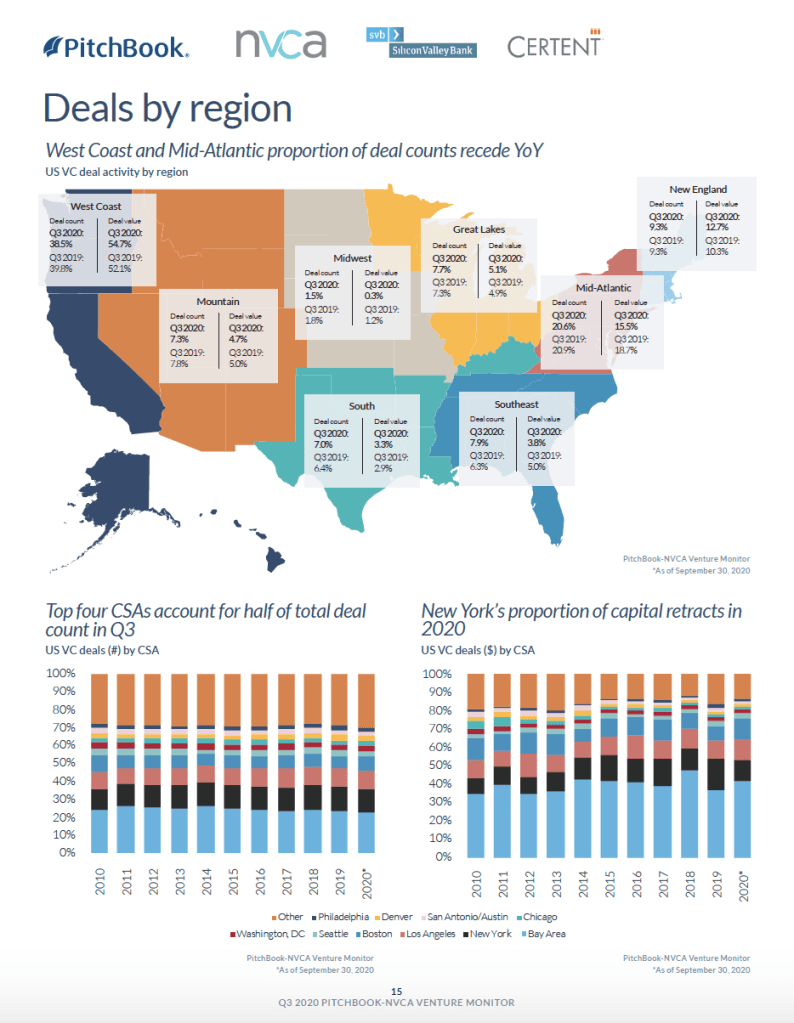

Take a look at the image below from the Q3 2020 Pitchbook-NVCA Venture Monitor report which provides a summary of the proportion of deals by region in the United States. Let’s start by looking at the West Coast. Deal count decreased 1.3% from 39.8% in Q3 2019 to 38.5% in Q3 2020. However, deal value increased 2.6% from 52.1% in Q3 2019 to 54.7% in Q3 2020. My immediate thought upon observing the data is that more capital is going to fewer (later-stage) companies as investors seek to support their “winners” during the pandemic. But what is also happening is that competition for deals in hotly-contested markets has increased valuations and investors have turned to other (smaller) markets to find new opportunities.

Look at the deal count and deal value in the South, Great Lakes, and the Southeast. In the South, both deal count and value is up YoY. I’m assuming this is mostly due to growth in the VC and entrepreneurial ecosystem in Austin, TX, where Apple, Google, and FB have recently opened offices. Similarly, the Great Lakes region also experienced a YoY increase in deal count and value. Chicago’s once fledgling VC ecosystem is now a contender on the national stage with firms like Hyde Park Ventures, BuildersVC, Chicago Ventures, and MATH Venture Partners. I’d be remiss if I didn’t mention Drive Capital in Ohio, one of the largest venture capital firms in the Midwest with over $1.2B in AUM across four funds. Per the company’s literature they state that “You no longer need to be in Silicon Valley to build a world class technology company.” Based on the data, I think a lot of investors are starting to agree with them.

The Southeast Region is probably the most interesting in that while there was a YoY increase in deal count, deal value decreased from 5.0% to 3.8%. Intuitively, I think this is due to a surge in investor appetite and growth in the number of seed stage companies, which generally don’t require a ton of capital to get started and they are competitively valued in comparison to East and West Coast companies.

While the struggle to find investors and source talent in smaller markets still exists, we’re witnessing a period in history where technological advancements and regulatory changes in how companies are financed (e.g. Jobs Act) are shifting geographic boundaries and expanding the scope for where and how investors and entrepreneurs source opportunities. This market shift has slowly been happening for the last few years and the pandemic has only accelerated and reinforced it. More research is needed to fully understand what the long-term effect on entrepreneurial ecosystems will be, but it’s been exciting to watch all of these changes happen in real time.

Cheers – KM

Hi Kevin – I hadn’t heard of your firm before today’s Pro Rata mention but got curious and came across this post. I don’t know if you’ll be adding new managers in your next fund cycle but based on your writing I suspect we have some shared views about where early stage returns are most likely to be found going forward. Give a shout if you ever want to compare notes and congrats on the success with the fund.

PS – here’s an analysis we did a while back, leveraging work from both Founder Collective and First Republic, on VC fund coverage relative to return in key North American markets: https://crashdev.com/2019/10/attention-returns-driven-lps-seattle-is-the-most-under-funded-early-stage-vc-market-in-north-america/

LikeLike

Thank you for sharing. Very interesting!

LikeLike